Credit Transmission Mechanism of Liberia’s Central Bank: Is it Pro-poor? (Theoretical Discussion)

By: Musa Dukuly (PhD)

suawantiwar@yahoo.com

The Perspective

Atlanta, Georgia

February 22, 2013

Credit Transmission Mechanism of Liberia’s Central Bank: Is it Pro-poor? (Theoretical Discussion)

By: Musa Dukuly (PhD)

suawantiwar@yahoo.com

The Perspective

Atlanta, Georgia

February 22, 2013

The ability of the poor to participate in the recovery and transformation of Liberia has been weak due to the absence of financial inclusion targeting women, youth and rural dwellers to earn living income. In recognition thereof, the monetary authority’s Financial Inclusion Program seeking to step up support to ease access to finance by Liberian owned businesses is the appropriate growth enhancing trajectory for tackling absolute poverty. As illustrated in Figure 1.0, this policy decision is critical for empowering the well-known poverty clients (lay-off workers, new college graduates, war affected women, returnees and rural dwellers). On this account, one may wish to ascertain the fundamental channels through which the credit program supports a genuine transmission mechanism for wealth creation and the attainment of middle income economy. Figure 1.0 shows the simple link and necessity of the pro-poor trickle-down of the credit intervention.

|

Looking at the simple conceptual framework, the monetary authority’s credit program via recycling of the 23.5 million USD will seemingly enhance “shared and inclusive growth” by promoting expansion of MSEs. Directly targeting the poor, which accounts for poverty incidence of about 60% or 2.1 million people, the 23.5 million USD (financial inclusion package) represents about 11.2 USD credit per every poor. Focusing on the empowerment of the poor, a flexible access to finance enables poverty clients to possibly escape poverty based on the marginal returns of capital, which is often high in low income country. Continuity of this policy in Liberia is imperative for sustained poverty reduction even at a stagnated or low economic growth. Indeed, the monetary strategy is pro-poor and aligned with the Brazilian growth paradox (2003-2010) where poverty was reduced by directly targeting the poor when its growth rate was still low.

It is also understandable that the current action of the monetary authority reflects commitment for pervasive economic diversification. Given the rational economic precept of the Central Bank of Liberia’s Governor that foreign investment alone is inadequate for rebuilding Liberia (Daily Observer, Vol.18, No. 879), it is generally discernable that a strong “Liberian Owned” private sector, supported by an effective credit program, is the appropriate roadmap for economically lifting impoverished Liberians and the country. This indeed suggests that the monetary authority is strategically on the practical pathway of accelerating the drive to Vision 2030 for an inclusive and shared growth. Its policy ensures that Liberia’s Ease of Doing Business rank (currently at 151 out of 183 in 2012) will likely improve via credit transmission mechanism to achieve self-employment, job creation and income distribution.

As a proportion of GDP (IMF estimates of 1.2 billion USD), the loan amount allocated by the monetary authority for Liberian owned businesses represents about 1.9 percent. In terms of distribution, the agriculture, housing and small/medium enterprises are the appropriate priority sectors because of their immense multiplier and growth effects. This indicates that many vulnerable MSEs shall have the opportunity to seek loan with flexible repayment duration and stumpy interest rate of 3/5years and 3 percent per annum, respectively. Compare to other African countries (Nigeria, Sierra Leone, etc), such a low cost credit policy will significantly boost penetration of MSEs in the credit market participation. Given the low absorptive capacity of the Liberian economy, the total loan amount as a proportion of GDP (i.e, 1.9 percent) is small, but could serve as a viable start-up to enhance financial deepening (i.e, credit to private sector), ensure wealth creation opportunity for the poor (especially the youth) and improve Liberia’s credit ranking (currently at 138 out of 183) in terms of ease of getting credit (World Bank Doing Business, 2011).

|

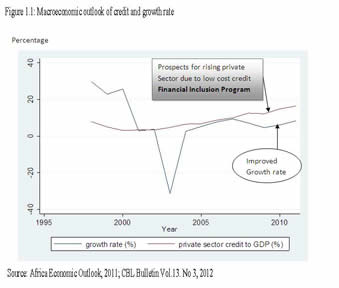

Source: Africa Economic Outlook, 2011; CBL Bulletin Vol.13. No 3, 2012

The indication suggests that the financial sector is gradually recovering to regain public confidence and ensure efficient credit delivery. If one examines the credit to GDP trend in Figure 1.1, one can surmise that the monetary policy is “aggressively” on course to genuinely enhance postwar Liberia’s transformation. The stimulus package for Liberian businesses is truly aggressive, and also healthy for reversing the fragile growth. This swift move of prioritizing extension of credit at low interest to small scale and other businesses is appropriate for slightly relieving the socioeconomic imbalance to enhance expansion of private sector (crowded-in effect). Moreover, this credit program seems robust and it is necessary for easing burden on household to meet other domestic pressing needs.

In terms of expectation, the pervasively low cost credit will certainly make a difference in the drive towards sustainable development. It will certainly help in the transmission mechanism of wealth creation to lift many Liberians from “appalling” poverty to “real” prosperity, especially the rural inhabitants. However, to ensure non-distortionary transmission mechanism of credit for broad base wealth creation, this credit program will require transparent credit unions, microfinance institutions and loan associations to effectively channel and manage the loans. In addition, the monetary authority should strive to provide the loan to credit institutions with consideration to entrepreneurship training and an improved credit infrastructure.

In concluding, the financial inclusion package of the monetary authority is certainly an integrated transmission mechanism to accelerate the attainment of pro-poor growth through increased production for employment creation. There is no doubt that the stimulus package offers a robust corridor for boosting the agenda for transformation by prioritizing the poor, which ensures self-reliance and self-actualization. If well implemented, the program could improve business cycle and immensely enhance poverty reduction. However, this financial inclusion program is likely to “marginally” reduce poverty in the first one-two years, but the cumulative effects could be overwhelming in the span of 5-10 years. So, the general preconditions are for the monetary authority to ensure that its policy aligns with easing restrictive credit requirements, strengthening prudential guidelines in regulatory systems, sensitizing borrowers, supporting a knowledgeable and growing entrepreneurial culture for continuity of the financial inclusion program.